AIR ANALYST NOTES

AIR116: WTO, Airbus Market Shares and Those Shiny Business Jets

Our topic for June are the WTO, Airbus and the resilience of business aviation, particularly in North America.

Our topic for June are the WTO, Airbus and the resilience of business aviation, particularly in North America.

This week, we provide an update for business jet production to 2030. Overall, the segment has demonstrated stronger than expected performance in terms of flight hours flown, primarily in North America and also production which was down only 18% from 2019…

As the the pandemic is unevenly subsiding globally, commercial air transport markets are beginning to recover strongly in North America, Europe and most of Asia. However, this growth hiatus will likely perdure into 2022-2023 for…

This research note is reserved content for AIR research clients only. Please login below and click on requested service to access content. Sign in to your AIR research account. Please ensure that the research note or forecast document that are you are trying to access is included in your current Read more

Much has been discussed recently about the beleaguered FCAS (Future Combat Air System). France and Germany are currently trying to find a solution before the end of April, ahead of the much-discussed Bundestag elections in September.. While the two parties appear to be deadlocked about FCAS work shares, and while the situation appears problematic to solve in the near term, some solutions are being developed to meet the crucial agreement deadline and ensure that prototypes and systems are on track for the second half of the decade.

This week’s monitor looks at some of the latest about Safran. The information is available directly on the AIR monitor landing page and to the Safran dashboard.

Our next Monitor will focus on Spirit Aerosystems.

We review some of the key stories for the week of March 1, 2021

This research note is reserved content for AIR research clients only. Please login below and click on requested service to access content. Sign in to your AIR research account. Please ensure that the research note or forecast document that are you are trying to access is included in your current Read more

This research note is reserved content for AIR research clients only. Please login below and click on requested service to access content. Sign in to your AIR research account. Please ensure that the research note or forecast document that are you are trying to access is included in your current Read more

Today’s conversation is centered around the issue of competitiveness of some of key NA commercial clusters post-pandemic. We are joined by Bruno Ferrand of Nect2US, Bruno has a long and distinguished career at Airbus and Latécoère.

It is clear that we are about to enter the most challenging phase of the pandemic crisis – consequences. A good dose of financial support was injected in the economies of Europe, North America and Asia in the spring/summer of 2020, but the tank is running low on those solutions.

Our key concern for the supply chain is the lingering effects of the government

In these market and highly volatile geopolitical environments, predictions for 2021 are complex. As Defense Secretary Rumsfeld famously coined: ‘unknown unknowns’ are simply piling up too fast and in too great numbers. The possible has become the probable and the situations, either political, societal or medical simply are too dynamic for analysts to precisely formulate a path forward

We host a discussion about 2020 and its far reaching consequences. This is part 1 of our annual review and outlook. The next note will focus on what we expect in 2021 in terms of production, market and competitive/supply chain dynamics.

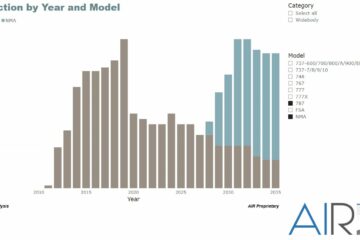

We have revised some of our numbers for the next five years. As outlined in our first briefing in April , 2020 to 2023 will witness a severe contraction, particularly for widebody markets. A slow recovery will materialize in the second half of the 2020s for that segment of the market.

Quick note. Let’s set the record straight – we are still calling it NMA, may be NMA light, but let’s use NMAv2 until the nomenclature is official.

News circulating that Boeing is again engaging with airlines in the definition of their future aircraft is really no surprise, it is actually a relief that customer engagement is moving from the tactical to the longer term. These interactions are frequent and are part of the ongoing conversation between OEM and customers.

What is however interesting is that Boeing is still pretty much following the Mike…

This research note is reserved content for AIR research clients only. Please login below and click on requested service to access content. Sign in to your AIR research account. Please ensure that the research note or forecast document that are you are trying to access is included in your current Read more

The world, and our aging United States appear to be under the influence of the “System of Doctor Tarr and Professor Fether” lately (aka the system of soothing – check your Edgar Allan Poe for an explanation). In between multiple customer engagements, our team sat down “virtually” last week to discuss the evolving crisis and attempt at striking a more positive and forward thinking tone about what lies ahead (yes, the Earth and the Sun do indeed continue their gentle cosmic dance and, as we like to say it often, “this too shall pass”).

This week’s note looks at the business aviation outlook to 2030. We have often connected the health of the business aviation market with other variables such as financial markets performance and corporate profits. Historically, there has indeed been a very strong correlation between aircraft orders and financial trends. However, the financial crisis of 2009 proved that this trend no longer applied…

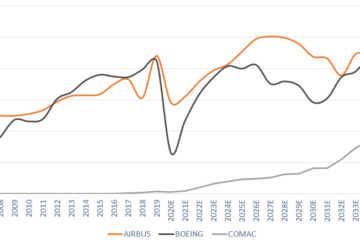

Production rates are a moving target these days. Boeing, Airbus, COMAC and Embraer have planned and adjusted production output based on anticipated demand recovery cycles, and which are based on a still rapidly evolving crisis. What happens in the next 6-12 months remains very

Airbus has announced significant cuts to several of its operations on 30 June , primarily in Europe for a total of nearly 18,000 jobs (including ADS), including 1,300 positions worldwide. This roughly matches Boeing and is in line with the severe contraction associated with the collapse of air traffic demand due to the current COVID pandemic.

Airbus also has other urgent issues to address, these are different from Boeing’s dire situation but those will need prudent responses if needed. While Boeing is currently severely impacted by the aftermath of its 787 and KC-46 development mismanagement and the current MAX regulatory and technical crisis, Airbus is faced with existing and potential challenges that will sequence themselves over a period of 15 years, and that may alter the course of the enterprise with varying degrees of severity.